There are a lot of steps that go into purchasing a home, and it’s normal to feel overwhelmed. Finally finding a house you love and making an offer is a huge step, but it’s only the beginning of the process to actually owning the home. It is important to familiarize yourself with what happens after making an offer on a house. Working with a credible expert is essential to making sure that you go through the process correctly, and ensuring that you don’t end up throwing money away on an offer that doesn’t go through.

What Happens After Making an Offer on a House

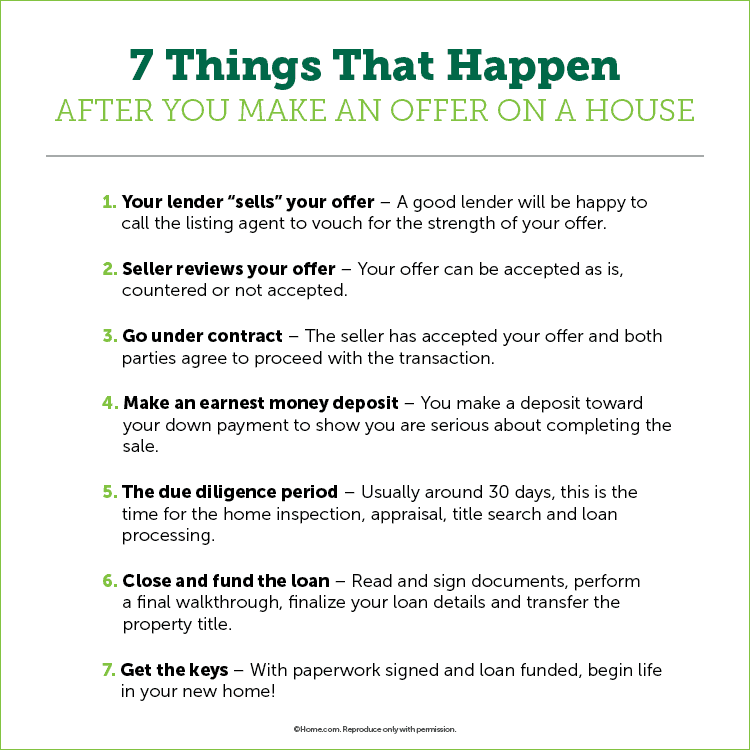

1. Get Your Offer Accepted

This probably seems obvious, but there are steps you can take to help your offer stand out and increase your chances of approval. Ideally you will be pre-approved with your lender before you put your offer in. Who you choose to work with can have as much impact on approval as your offer amount. A good lender will have already vetted you thoroughly for pre-approval and will be happy to contact the listing agent on your behalf. Your loan officer should provide the listing agent with not only your credentials but theirs as well. The timeline and reputation of your lender can give you an edge even if your offer isn’t the highest.

2. The Seller Reviews Your Offer

You will submit your offer (via the purchase and sales agreement) and it will be reviewed by the listing agent or the seller’s attorney. They will review it with the seller.

At this point, the offer will either be accepted, a counter offer will be made with changes to the offer, or the offer will be denied outright.

Usually your offer will be presented to the seller quickly and you’ll receive a response within 24-48 hours. It may take longer if the seller is reviewing multiple offers. Their agent should give you some idea of the expected timeline.

If there are multiple offers, you may be rejected for not being the highest offer. You are more likely to be accepted or receive a counter offer if there are less offers, or if you are the only one. You may be able to make a counter offer with a higher amount, or you may need to accept the loss and start over on a different home.

3. Go Under Contract

If your offer is accepted, the sale contract and purchase agreement will be updated to reflect any changes in negotiated terms. Both you and the seller will sign it. This is known as “going under contract” and means that both parties have agreed to move forward. At this point the seller cannot show the home to anyone else, as they have agreed to sell it to you, provided closing terms are met.

You may feel some buyer’s remorse or anxiety at this point. Making an offer can feel like a whirlwind process, especially if you are bidding against other buyers. This feeling is normal, but typically passes.

4. Make Your Earnest Money Deposit

Once you are under contract, you’ll typically want to send your escrow deposit to hold the contract. This deposit shows that you are serious and will go toward your down payment and closing costs down the line. This amount includes your earnest money fee, an amount agreed upon to indicate your commitment to the sale. Keep in mind that if you break the contract, you risk losing this deposit. If you meet the terms of the contract but cancel for a valid reason, you should get your deposit back.

Depending on where you live, you may also be asked to supply a due diligence deposit. Due diligence fees give the seller extra protection during the due diligence period where you have the home inspected and appraised, and during which time the seller cannot show the property to anyone else. This deposit is non-refundable unless it is the seller who cancels the sale.

5. Make the Most of Your Due Diligence Period

Once you are under contract, the due diligence period begins, and can last anywhere from 7 to 30 days. During this period, the buyer or seller can opt out of the contract without penalties, so long as those conditions are detailed in the contract. There are a few specific steps that you will take during the due diligence period.

First, the home inspection. This isn’t mandatory but it is highly recommended that you hire a professional home inspector to conduct a general inspection. They will check every area of the property and point out any problems. You may also request additional inspections such as an air radon test, air mold test, inspection for things like termites, and property scans for oil tanks or anything else that may be buried on the grounds. If any significant problems are found, you can negotiate with the seller to either lower the price or have repairs completed before closing.

Next is the appraisal. This is paid for by you, the buyer. The appraiser will do a review of the property on-site, then complete a detailed breakdown of the property’s worth. They will compare the home to similar properties to establish its worth.

Ideally the appraisal will find that property value closely matches the purchase price. If they find that the property is worth less than the purchase price, your lender will typically revise the loan amount to only cover the appraised value. At that point you may have to find another way to cover the difference, or go back to the seller and attempt to negotiate based on the appraisal.

A title search is also paid for by you, and ordered by your attorney or agent. The title search will determine whether there are any legal barriers to you taking ownership of the property or any legal concerns that could lower the property’s value. It will show any liens on the property, easements, covenants, or any restrictions that you may need to abide by as the new owner. You can also have a municipal title search which will show any closed or open permits that have been granted for the property.

Finally, your lender will process your loan application with any revisions based on the appraisal or contract changes. You will likely be asked to provide the same documentation you handed over for pre-approval, including pay stubs, tax returns, bank statements and other financial records. This will be sent to the underwriting team, who will carefully go over your finances and loan details. Underwriting will also review the appraisal report and title information.

6. Closing and Funding

At closing, the property title transitions from the seller to you. You may perform a final walk-through of the property, and fill out several more required legal documents along with the seller.

Three days before closing, you’ll receive an initial closing disclosure to review. This includes all of the details of your loan, including repayment terms and other important information. If you have any questions, be sure to go over them with your loan officer before you close. Once you’ve signed the loan documents you are responsible for fulfilling the loan as written.

The loan becomes official when the mortgage loan is funded, with funds distributed either by both parties’ attorneys or by a title or escrow company, depending on your location. At this point the sale is finalized.

7. Get Your Funding Date and Then Your Keys

The title company closing agent will gather all of the signed documents and money from all parties. They will then notify all parties that the loan is officially complete. At this point the home ownership changes from the seller to the buyer.

Your loan officer will tell you when your funding date is. It is often on the closing date but may vary, especially if you close on a Friday or late in the day. Only once the loan is funded, and the new deed and ownership records are updated with your county, do you take possession of your keys.

Hopefully you feel less overwhelmed learning more about the specific steps that take place once you make an offer. Home buying can be complicated, with a lot of new terms to learn and rules to follow. This is why it is so important to work with a credible lender who can help walk you through the process all the way from having your offer accepted to closing.

Planning to purchase your dream home? Get the right information and assistance from Fairway’s First Team’s Home Buyer’s Checklist. You’ll find a comprehensive range of financing options and diverse mortgage advice. https://t.co/PkG2PdhcGN home-buying-checklist pic.twitter.com/pS1enDdaCA

— FairwaysFirstTeam (@FairwayImco) March 11, 2022