An FHA loan refers to a mortgage loan insured by the Federal Housing Administration, which is run by the Department of Housing and Urban Development (HUD). These loans are offered by the United States government to help make home ownership more accessible for those with lower credit scores and who may not be able to afford larger down payments. Prior to the introduction of FHA loans, potential buyers without stellar finances had a much harder time securing mortgages.

FHA loans are especially popular with first-time home buyers. If you’ve been dreaming of owning a home but limited by your credit score or limited savings, an FHA loan could help you reach your goal. Keep in mind though that FHA loans have some downsides that conventional loans don’t, most notably the requirement of mortgage insurance for the duration of the mortgage.

Are you a first-time homebuyer looking for an FHA mortgage loan? Why not go with the best mortgage lender for FHA loans in 2020? Fairway’s First Team are committed to top-notch service when financing your new home. Click or call (503) 765-1150! https://t.co/g12ZDMnTJC pic.twitter.com/bhq0JRSaJh

— FairwaysFirstTeam (@FairwayImco) March 14, 2022

So what are the requirements for an FHA loan?

FHA Loans Income Requirements

While there is no set income requirement for an FHA loan, you will need to show that you can afford to make the monthly mortgage payment. Your lender will need documentation of your income to move the loan into the underwriting process for approval. They will also need your income to calculate your DTI, or debt-to-income ratio.

Possible proof of income could include:

- Pay stubs or W2s

- Profit and loss (P&L) statements documenting freelance or gig work income

- Bank records documenting investment or other income

- Social security, disability, or SSI award letter

FHA Loans Employment Requirements

When you apply for an FHA mortgage, as with any mortgage loan, your lender will ask to see a minimum of two years of employment history. That could mean pay stubs or tax records if you have worked for the same employer for at least two years.

If you are self-employed, you’ll need to provide at least two years of personal and business tax returns. You may also be asked to provide profit and loss (P&L) statements and/or other financial statements for your business. You may be able to qualify after only one year freelancing so long as you have at least two years’ prior experience in the same line of work. If you recently completed college and just started working, your degree program may be able to count toward your work history.

A stable job and income are the most important factors towards qualifying for an FHA mortgage. The better you can demonstrate that you can afford your monthly mortgage payments, the better your chances at being approved by a lender.

FHA Loans Credit Score Requirement

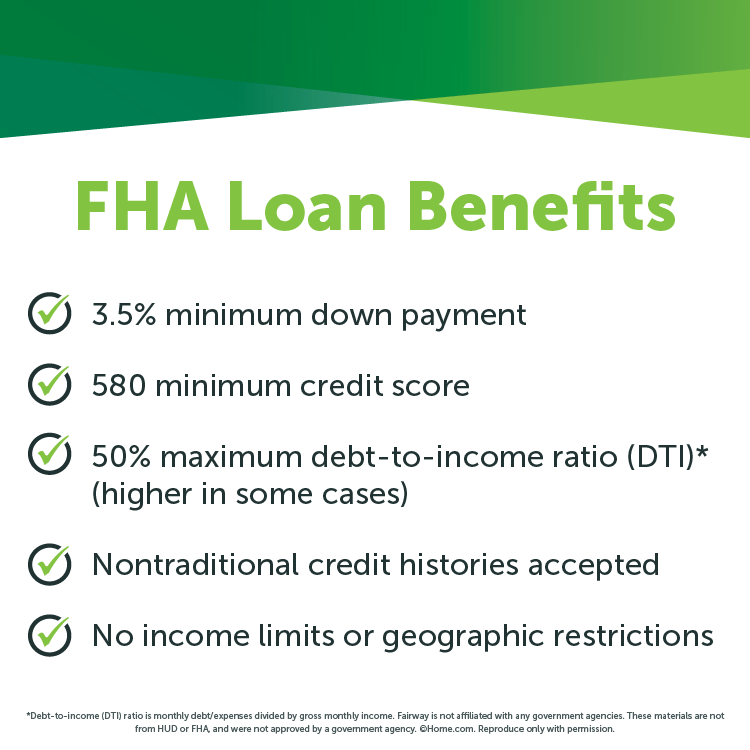

The minimum credit score requirement for an FHA loan is 580. (You may be able to qualify with a minimum credit score of 500, but the minimum down payment will be higher. Not all lenders will work with a credit score under 580.)

Your lender will run a credit check when you apply for preapproval. This may include a small fee – usually around $30 or less – to cover that cost.

If you don’t have a credit score, that’s OK. FHA loans don’t require that you have a traditional credit score. Instead, your lender will typically ask for documentation of making rent, utilities, and other monthly payments on time. Without a credit score it will be even more important that you can demonstrate your stable employment and sufficient income.

FHA Loans Down Payment Requirement

The minimum down payment for an FHA loan is 3.5%. If you are unable to come up with that down payment on your own, you may use gift funds to cover the difference. The gift amount could come from a variety of sources, including friends or family members, your employer, certain charities, or approved down payment assistance programs.

You cannot use cash for your down payment, as lenders need to see a paper trail documenting the source of the money. You will need records of all deposits and money transfers. If you are using gift money, you will also need a signed letter from the gifter verifying that it is in fact a gift and they do not expect repayment.

FHA Loans Eligibility Requirements

FHA loans are available for U.S. citizens, both permanent and non-permanent resident aliens, and Deferred Action for Childhood Arrivals (DACA) recipients. You must also be eligible to work in the United States and have a Social Security number.

The home for purchase must be your primary residence, not a second or investment property, and you must meet all of the other FHA loan requirements.

FHA Property Requirements

As with all mortgage loans, an FHA loan will require an appraisal. An FHA loan requires sign-off from an FHA-approved appraiser, ensuring that the home you want meets the minimum property standards. Your lender will hire a qualified appraiser.

The FHA appraiser will look for the following:

- Adequate living space

- Structural integrity

- Access to drinkable water

- Adequate heat, hot water, sewage disposal, and sufficient electricity

- Minimum one bathroom with a toilet and a bath or shower

It is worth noting that after the 2000s housing crisis, most condo complexes were removed from the FHA’s approved condo list. Many never got re-approved. You can use the HUD website to search for approved condo properties.

FHA lenders can only approve a loan if the appraisal matches the offer price. They cannot approve a loan if there are any major structural or life quality issues. You will want to discuss these issues with your real estate agent before making an offer. If there are any issues, the seller may be willing to fix them before the FHA appraisal.

FHA Loan Limits

Every year the FHA publishes a list of loan limits based on median housing prices. The list includes a floor and a ceiling amount. The floor is the maximum loan amount allowed for the most low-cost housing areas in the country. The ceiling is the maximum amount for high-cost areas. Alaska and Hawaii have their own limits which are even higher.

How much you are entitled to borrow depends on the housing costs in the area where your potential home is located, and the difference between those limits can be extreme. You can use the mortgage limits search tool on the HUD website to find out what the limits are in your desired location.

FHA Loan Closing Costs

The amount you will pay in closing costs depends on the amount you are borrowing and where you live. The average closing costs in 2020 were $6,087 including taxes according to ClosingCorp (closing.com), although that number can be a lot higher depending on your location. You can generally expect to pay about 2.5% of your loan amount in closing.

No matter what your location, you will need to budget in closing costs. You may be able to get a closing credit from the seller or from your lender, but your home price or interest rate will end up being higher.

An estimated breakdown of closing costs:

Loan origination fee – 0-1% of the total loan amount

Application fee – $300

Appraisal fee – $500

Home inspection fee – $300

Pest inspection – $100

Homeowner’s insurance – $300-1000

Title search and insurance – $900

Credit check fee – $30

Attorney fee – $500-1000

Survey fee – $150-400

This is not a complete list of closing costs. Other fees include prepaid taxes, as well as additional inspections mandated in your area. Your lender is legally required to supply you with closing disclosure documents three days before closing. These documents will outline all of the fees and expenses you owe. You are encouraged to look these documents over closely and ask any questions.

FHA Mortgage Insurance Requirements

An FHA loan requires that borrowers pay a mortgage insurance premium (MIP) throughout the entire life of the mortgage loan if they put down less than 10% as a down payment. (With a conventional mortgage, MIP is only required until you reach 20% of the home’s equity.)

Borrowers first pay an upfront MIP equal to 1.75% of the loan. This is paid upfront and is usually wrapped up into the loan amount. You have the option to pay it with cash, or using any available closing credits or assistance. Typically though it is included in the loan amount.

After the upfront MIP payment, borrowers will continue to make monthly mortgage insurance payments. Annual mortgage insurance premiums vary between 0.45% and 1.05% annually. Borrowers with a down payment of more than 10% are only required to pay MIP for the first 11 years. Annual MIP payments are broken down into monthly payments and included with your monthly mortgage payments.

Once you have reached 20% in home equity, you can refinance your FHA loan to a conventional mortgage. As stated before, conventional mortgages require PMI on loans with less than 20% equity.

FHA Debt-to-Income Requirements

Debt-to-income ratio (DTI) is the term for the percentage of your gross monthly income that goes towards debt payments. Debt payments are anything that was taken out on credit – car payments, student loans, and credit cards as some primary examples. Your DTI does not include things like rent or phone bills which are monthly payments but do not involve taking out a line of credit.

There are two types of DTI, referred to as front-end and back-end.

Front-end DTI includes your estimated mortgage payments, including interest, mortgage insurance premium, taxes and fees.

Back-end DTI includes all of your monthly debts, including your mortgage plus any credit cards or other debt accounts, including car payments, student loans, personal loans, back taxes, or anything else that is paying off a line of credit.

Ideally for an FHA loan you will want a back-end DTI of at or below 45%. Many lenders, though, will approve a loan with a DTI of 50% or more as long as they receive an approval from the FHA computerized system. About 25% of all FHA purchases in 2020 were by borrowers with a DTI above 50%.

To calculate your own DTI, add up all of your monthly debts as explained above (anything that is paying off a line of credit). Do not include any non-debt payments. Take that sum and divide it by your monthly income before taxes. That is your debt-to-income ratio.

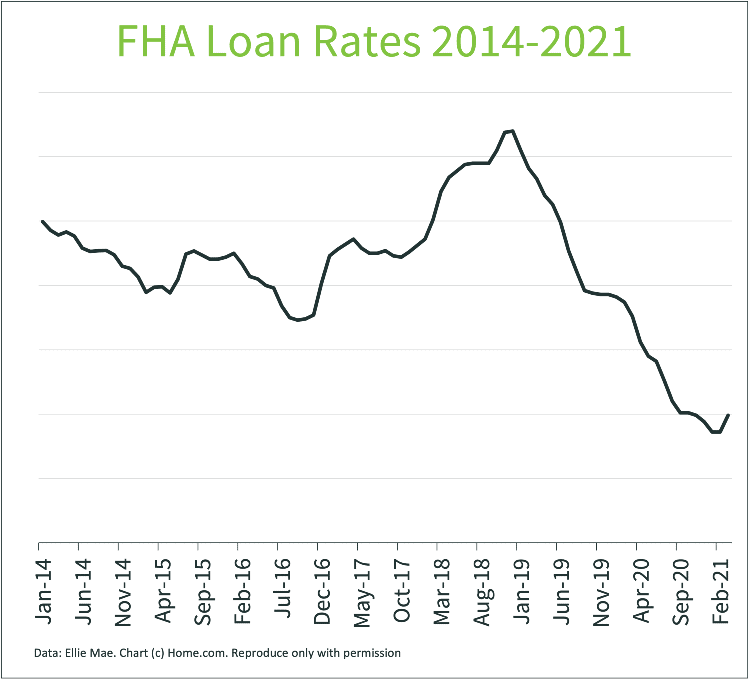

FHA Loan Interest Rates

Mortgage interest rates hit historic lows in 2020. They are slowly rising again, but likely to stay fairly low for a while. Your mortgage interest rate is based primarily on your credit score and how much you are looking to borrow. Less money being lent is less risk, and lenders see borrowers with higher credit scores as more likely to repay the loan. Keep in mind that instant quotes online may not be especially accurate. The only way to find out your true borrowing power is to see a lender and get preapproved.

FHA Loans for First-Time Home Buyers

Many first-time home buyers can afford monthly mortgage payments but have a hard time saving up money upfront for a down payment. The flexible credit and DTI requirements, and especially the low down payment option, may make an FHA loan the best – or the only – option. According to HUD, more than 80% of FHA loans go to first-time buyers.

First-time home buyers should understand and consider all of their possible loan options. You should request quotes from multiple lenders and go with the lender you trust, not necessarily just with the lowest quote. If you decide on an FHA mortgage, make sure you choose a lender that has ample experience with FHA loans.

Pros and Cons of an FHA Loan

- FHA Pros

- Low credit score requirements

- Lower down payment requirement

- No strict income limits

- Higher DTI limits

- FHA Cons

- Monthly and upfront MIP (Mortgage Insurance Premium) payments

- Property restrictions

- Not available for second homes/investment properties

Choosing a mortgage is a big decision and it’s a good idea to consider all of your options. Finding a lender whom you trust can help make the decision less scary. Preapproval will give you an idea of how much you’ll likely be able to borrow and which loans you can qualify for. You can then use that information to start getting your finances where they need to be, if necessary, and start looking at homes. If you can afford mortgage payments but are having trouble coming up with enough for a down payment, an FHA loan may very well be for you.